Property News

Why House Prices Are Rising In Spain (It’s not a bubble)

According to numbers that have come out of the National Statistics Institute (INE) of Spain, the housing market here continues to boom and prices continue to rise. Some commentators have suggested there is a bubble forming.

Others however, including researchers at Caixa Bank, think that the rise in prices has less to do with a speculative bubble and more to do with other factors.

On September 5, 2025, a major article came out in El Pais announcing that the price of second hand homes had surpassed the prices reached during the 2007 bubble, just prior to the crash. The price of new homes had already surpassed this level in the fall of 2020.

This is obviously a psychological indicator because the housing collapse was deeply traumatic in Spain, which was one of the worst hit countries in the EU.

Surpassing this milestone is viewed both good and with trepidation – especially as the prices keep on rising, as El Pais notes:

“The general index, driven primarily by the performance of second-hand homes —which are the majority in both quantity and number of transactions—grew 12.7% compared to the second quarter of 2024, the largest increase since 2007. It has now seen 45 consecutive quarters of year-on-year increases, just over 11 uninterrupted years of price increases.”

This does indeed seem like a shocking growth in prices over a very long period of boom. Prices, on average, are now 78% higher than they were in 2014 when the housing market reached bottom and began to recover.

On the Costa del Sol, in Marbella, prices have increased by 9.8% in the last year, which is less than the national average but from a much higher level. At €5,162/metre, Marbella real estate is twice the price of the national average.

However, there needs to be some caveats and some perspective when we look at Spanish real estate prices.

First of all, the increase in prices beyond their levels prior to the 2008 crisis is in nominal terms, not in real terms, according to a research paper by Caixa Bank. That is, when we account for inflation, the price of second hand homes is still 23% lower than their peak in 2007.

The picture is slightly different with new homes, which have risen above pre-crisis levels in real terms in the Balearic Islands, Andalusia, the Canary Islands and Madrid. In the rest of the country the picture is similar to that with second hand homes.

The Perfect Storm

Additionally, we need to keep in mind that the underlying reasons for the growth in prices are very different than in 2007. Then, the rapid increase in prices was steeper and was driven by speculation and debt. And because it was driven by speculation, there was over-construction of homes with no buyers – there was a mismatch of too much supply for not enough demand.

This time, it is the opposite.

The Spanish population is growing and will soon pass 50 million people – that’s ten million more than at the start of the 21st century. This is largely due to immigration, as Spanish-born people are not having babies at anywhere close to replacement rate.

To maintain a growing workforce, pay for social services and pensions for Spain’s baby boomers – and a growing economy – Spain has become a country of mass immigration. For several years immigration has been at a level of approximately 1% per year, similar to countries such as Canada.

That has created a conundrum. On the one hand, Spain needs those immigrants or the economy would stagnate – or worse. On the other hand, no government at any level has instituted the policies needed to dramatically increase housing construction to meet the growth in need.

The result is too many buyers chasing too few homes. According to a spokesperson from Fotocasa, quoted in El Pais: “of citizens who interact with the buying and selling market, 81% want to buy, compared to 12% who sell.”

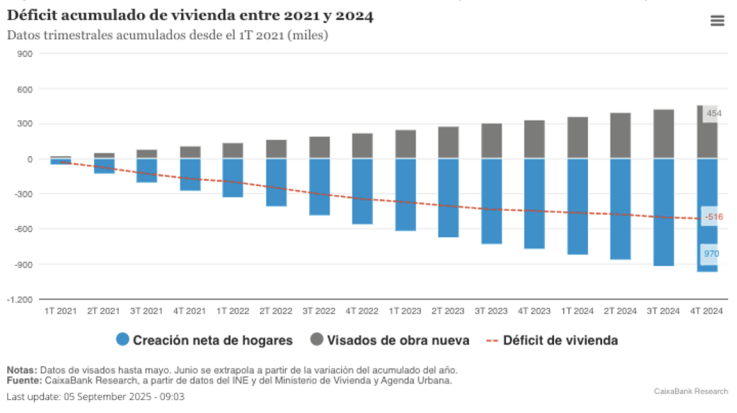

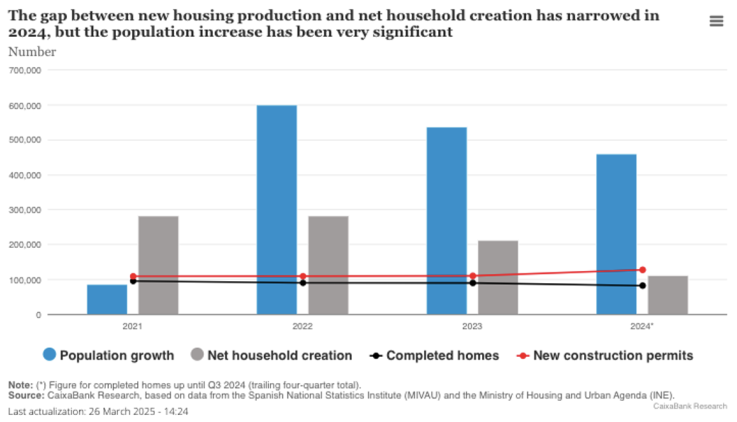

Another Caixa Bank study, found that since 2021 the deficit in home construction – that is, the number of new houses built vs the number of new households formed that need them – has grown from 33 thousand to over half a million in total (see Caixa chart below).

That’s a huge and obviously unsustainable increase. And it is driving the protests demanding affordable housing that have spilled over into calls for restricting tourism and tourist housing.

The housing deficit has also grown in a context that has created a perfect storm for price inflation. In the immediate aftermath of the Covid lockdowns, Spain had low debt levels and higher savings than for many years. When the lockdowns ended, there was pent-up demand that led to a surge of house purchases.

That has been followed by waves of interest rate decreases over the last year, mortgage rates are back below 3%, with the European Central Bank prime rate barely above 2%. That has helped to keep domestic demand up after the passage of the post-Covid surge. According to the first Caixa Bank study quoted above, the number of mortgages increased by 11.2% in 2024.

On top of these structural elements there has been a growth in foreign home purchases in Spain. According to the article in El Pais, house purchases by foreigners have reached 18% of all purchases.

As a result, if we count the number of completed homes destined to be purchased by buyers living in Spain, the housing deficit is even worse. Caixa Bank says that the rate of construction between 2020-2024 has only met 20% of the country’s actual housing needs, leaving a deficit of not half a million but a massive 765,000. This is estimated to be at the root of 40% of the price increases.

No Construction

Ultimately, the real source of the problem is very straightforward – if not the solution. Spain isn’t building enough homes. This is a problem that emerged after 2007 when there was a massive wave of bankruptcies.

Often, construction companies would go bankrupt, leaving empty developments of half-completed homes. Banks were forced to take them over and became saddled with billions in bad debt and hundreds of thousands of foreclosed homes.

The government responded by saving the banking sector but at the cost of restricting paths to recovery for the construction sector. Loans became harder to get, capital requirements more stringent. For a decade new housing construction was flat-lined, dead in the water.

In the immediate aftermath of Covid, the surge in inflation also affected construction materials. So, while there was a housing boom, it was almost exclusively in second hand homes.

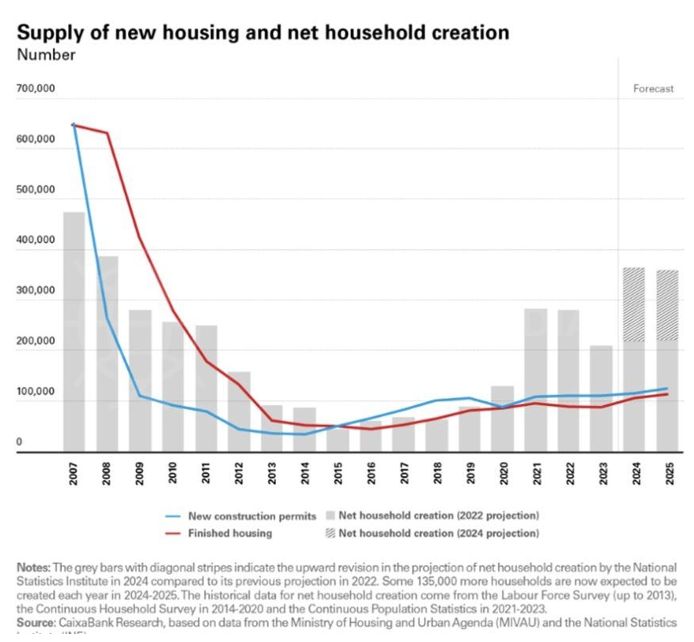

There is good news in all this. While the current growth in prices is posing a challenge for house hunters, there is a growth in the number of housing starts. Permits for new homes grew by 16.7% last year and for the first time since 2018 surpassed the rate of new household formation. That trend is expected to continue and will ease pressure on the housing market over the coming years.

Secondly, while the price increases look dramatic, they are largely confined to the Mediterranean coastline and Madrid. Over the country as a whole, the price of housing is increasing in line with income growth and the affordability ratio has barely budged.

That doesn’t mean that there’s not a problem that needs addressing. There clearly is. But it means that there is light at the end of the tunnel.

Ultimately, it is better to be “cursed” with unbalanced growth than with a balanced collapse in demand. It is easier to adjust an economy that is moving forward than one that is in retreat.

By Adam Neale | Property News | October 2nd, 2025

Related Posts