Taxes and fees for landlords

When renting a property, landlords may be obliged to pay a variety of different taxes, depending on their status and the type of property in question, as well as the cost of any fees owing to third parties

Renting out property on the Costa del Sol, either to long-term tenants or to tourists for short-term stays, can provide good returns on investment for owners and investors who want to become landlords, but, as with all income earned, taxes are due on any gains you make. To work out exactly what you’ll owe, we asked Adolfo Martos of the Marbella-based legal firm of Martos & Gross Abogados, for the details of Spanish taxation law.

Income Tax – What you will pay if you rent short or long term depending upon your resident tax status

Tax Resident in Spain:

If a landlord is a private individual and tax resident in Spain, you are required to declare any earnings from rental properties on your annual declaration of income tax (IRPF or the Impuesto de Renta de Personas Físicas, in Spanish). The amount of tax you pay will depend on the total amount you earn during a fiscal year, although a number of deductions can be offset against gross income earned from rent.

Applicable deductions include maintenance costs, annual depreciation, mortgage interest, community charges, municipal property taxes, refuse collection and similar outgoings, Adolfo explains. And when a property is rented to tenants for use as their primary residence, landlords are permitted to reduce net profits (income earned minus costs) by 60%.

When the landlord is a Spanish company, the same principles apply to net profit earned from rental properties. Profits are taxed at the standard corporate tax rate of 25%, unless the company is newly established, in which case a reduced rate of 15% applies to taxable profits for the first two years of operation.

Non Tax Resident in Spain:

If the landlord (private individuals and companies) is not resident in Spain for tax purposes, the amount of tax due in Spain depends on where you habitually pay tax. If you’re tax resident in the European Union, you are required to pay 19% of net income, Adolfo points out, whereas if your fiscal residence is outside of Europe, the fixed rate is 24% of gross income, as the deductions described above are not applicable. In either case, you are required to declare income and pay tax on a quarterly basis, using the 210 model form.

VAT – is due when you rent short-term for tourists, with hotel-like facilities

If you rent your property to the public and provide services then in principle you are obliged to charge VAT. The reality is very few people know this fact and even fewer charge but in theory as a landlord you are liable. When a property is rented under a short-term contract for tourist accommodation and the agreement includes services, such as changing linen and cleaning, landlords are, conversely, not required to pay TPO (see below) but to charge tenants VAT at a fixed rate of 10%. So, if you plan to rent a property for a week at a daily rate of 100€, the total amount per day you should charge is 110€. On a quarterly basis, landlords are required to settle accounts with the tax authorities by submitting VAT form 303, which reflects both output VAT (paid by tenants) and input VAT (paid by landlords for services related to the property).

TPO – is due when you rent long-term to private tenants

Generally no one pays this but in principle every landlord should pay it, especially since it is such a small amount. If you intend to rent a dwelling to tenants for their own use under a long-term contract, Adolfo says that what you charge for monthly rent is exempt from VAT (IVA, in Spanish), but is subject to a taxable asset transfer levy (known as TPO, or the Impuesto de Transmisiones Patrimoniales Onerosas). The amount of TPO you are liable for is calculated on the taxable base of rent payable over the term of the contract.

Depending on the terms of the contract, conditions may apply, Adolfo notes: i) if the duration is specified, you need to sum up the total rent to be paid; ii) if duration is not specified, you have to calculate the amount to be paid over a period of 6 years (and, should the contract be extended for a longer period, pay additional taxes); iii) if a property is a tenant’s primary residence, the taxable base cannot be less than the sum of 3 years’ rent.

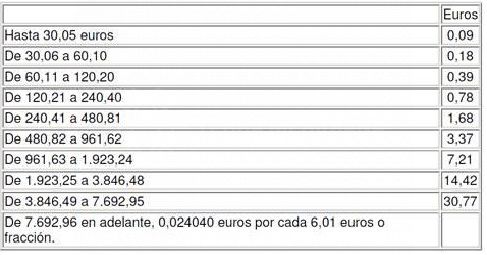

Once you’ve calculated the taxable base, the amount of TPO owing is levied in line with the following table:

As an example, Adolfo explains, if you calculate the total amount of rent payable over a three-year period at 43,200€, the TPO you would be obliged to pay is 173€. Landlords, he adds, are held liable to pay TPO if the tenant does not provide proof on payment at the same time as payment of the first month’s rent is made.

Agency Fees: What it costs to rent with Terra Meridiana

At Terra Meridiana, we have more than a decade and a half’s experience letting property on the Costa del Sol, working on behalf of private homeowners and company landlords. We provide comprehensive, all-inclusive property management services that offer owners and investors total peace of mind, from marketing to managing short-term stays and long-term tenancies, at competitive, fixed-rate fees.

For short-term lets, such as tourist accommodation, we charge 20% of the total rental price, plus 21% VAT, including: advertising your property on our own and international websites, handling contracts, holding and returning deposits (if applicable), meeting and greeting clients, checking out, revising inventory and the state of the property upon exit, and being responsible for any client-related issues throughout their stay.

For long-term lets, we charge the equivalent of one month’s rent, plus 21% VAT, including: advertising the property on Terra Meridiana’s and third-party websites, sourcing and selecting suitable clients, checking tenant references and solvency, contractual negotiations, and taking responsibility for any tenant-related problems that may occur during the term of the tenancy.

Special Tax Cases for Landlords:

Renting new properties or properties with an option to buy

Rental contracts for brand-new properties are always subject to payment of VAT at 10% rather than TPO, Adolfo says. But when the contract includes the possibility of purchasing the property (opción de compra in Spanish), the following taxes may be applicable:

If the owner/grantor is an entrepreneur acting in business he is required to charge the tenant an additional 21% in VAT on top of the price paid for the right to the option (also known as the option premium).

In case the owner/grantor is not an entrepreneur acting in business, then the option is not charged with VAT but with Transfer Tax payable by the option holder.

Renting properties for subletting purposes

When a property is rented to another party with the intention that it subsequently be sublet to third parties, VAT is due at a rate of 21%, Adolfo notes. An example would be the owner of an apartment in a managed complex who rents the property back to the management company for them to sublet it to other people, such as the Pierre et Vacances or Marriott business models in use on the Costa del Sol.

In this case, the property owner would be obliged to charge the management company 21% VAT on top of the rent payable for the apartment. So, if the company agrees to pay an annual rent of 5,000 Euros, the invoice issued by the owner to the company should be 5,000€ plus 21% VAT. Any rental services (maid service, etc.) provided by the management company to tenants is exempt from VAT, but subject to TPO, as the property would be rented by them to the final user, I.e. the tenants.

Special Tax Cases for Tenants:

Renting with a registered contract – an option for tenants

There are instances where it is advantageous for a tenant to insist their contract is registered with the Property Registry, such an instance may be for example in the case where the tenant is expressly interested in an option to purchase the property. If a landlord and tenant agree to register their contract with the Property Registry, in cases where VAT is applicable, Adolfo says the owner is also liable for Stamp Duty (Impuesto de Actos Jurídicos Documentados or AJD in Spanish) on the notarial documents required, at a fixed rate of 1.5% of the total value of the contract. That includes the sum of all rent to be paid over the agreed duration of the agreement and, if there is an option to buy in the contract, the option premium or 5% of the purchase price agreed, whichever is the highest.

Alex Salazar

Email

+34 951 318 480

Related Posts